A CFO at a mid-sized logistics company opens ChatGPT and types: “What’s the best embedded payments platform for B2B invoicing?” The AI responds with three names. Yours isn’t one of them.

It’s not a product problem. Your platform handles the use case. It’s a GEO problem — your site holds the regulatory credentials, the compliance documentation, and the product depth that AI models are supposed to trust. But the technical signals required to communicate that trust are missing, misconfigured, or inaccessible to the crawlers that feed those AI responses.

Check your GEO score in under 60 seconds. No signup. No cost.

✅ Free ⚡ Results in 60 seconds 🔒 No signup required

GEO Score Checker

Your Compliance Credentials Mean Nothing If AI Can’t Read Them

Fintech brands operate in the highest-scrutiny category for AI search: YMYL (Your Money or Your Life). That means AI models apply their strictest verification standards before citing a financial services brand. The brands that get cited aren’t always the most credentialed. They’re the ones whose credentials are structurally accessible to AI crawlers.

That gap is measurable.

Scenario 1: A Licensed Lender Blocked by Its Own Robots.txt

A B2B lending platform carries a full NMLS license, publishes quarterly compliance reports, and maintains a detailed FAQ on regulatory coverage. Its Bot Access score: 18 out of 100.

Why? A misconfigured robots.txt file blocks GPTBot and PerplexityBot from crawling the compliance section entirely. From the AI’s perspective, the lending credentials don’t exist. A competitor with weaker regulatory standing but an open crawl path gets cited instead.

Scenario 2: Schema Markup That Doesn’t Speak Finance

A payments infrastructure provider has deployed basic Organization schema. But its product pages lack FinancialProduct schema, LoanOrCredit schema for its credit facilities, or any JSON-LD fields encoding riskLevel, regulatoryBody, or licenseNumber. The Structured Data score reads 29.

AI models can see the product exists. They can’t verify what it is, what regulatory body oversees it, or how it compares to alternatives. In a YMYL context, that ambiguity is disqualifying.

Scenario 3: Visible on ChatGPT, Absent on Perplexity

A wealthtech platform ranks well in ChatGPT responses because it’s been cited in American Banker and Banking Dive, sources that ChatGPT weights heavily. But on Perplexity, which leans toward community sources like Reddit’s r/personalfinance and r/fintech, the brand has no footprint. Its Visibility Score reflects the split: strong on one platform, invisible on others.

This is a platform distribution problem, not a content problem. And it won’t show up in your Google Analytics.

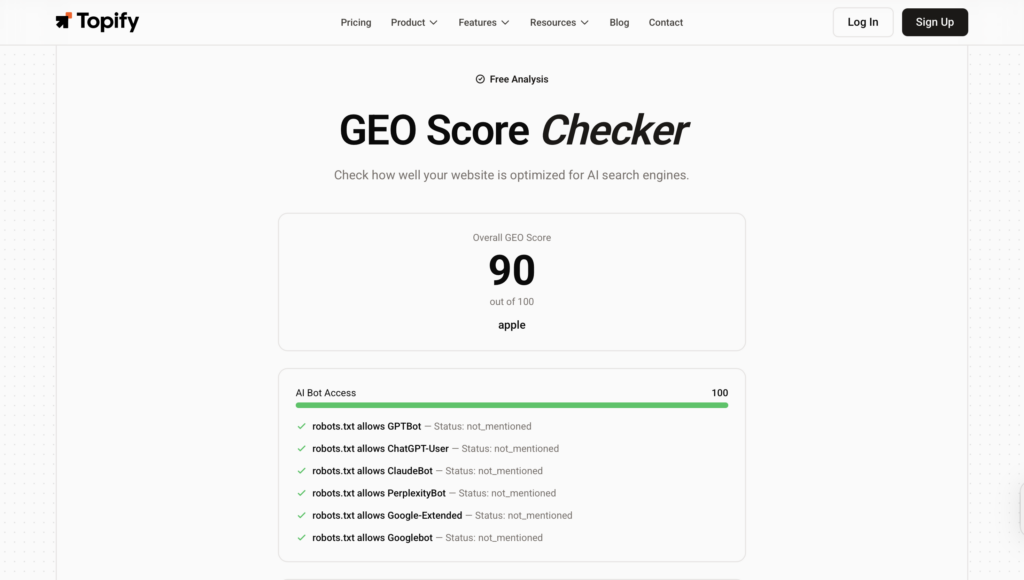

The Four GEO Scores That Decide If AI Recommends Your Fintech Brand

Topify’s GEO Score Checker runs a four-dimension diagnostic on any fintech domain. Each score targets a different layer of AI citation readiness. Here’s what each one means in fintech terms:

| Score Dimension | What It Measures | Fintech Impact |

|---|---|---|

| Bot Access | Whether AI crawlers (GPTBot, ClaudeBot, PerplexityBot) can access your site | Compliance pages, product specs, and licensing data become invisible if bots are blocked — even partially |

| Structured Data | Quality and completeness of schema markup | Fintech requires FinancialProduct, LoanOrCredit, and Organization schema with regulatory metadata; generic schema fails YMYL verification |

| Content Signals | Semantic authority and E-E-A-T signals in your content | Named credentialed authors (CFA, CFP), inline disclaimers, and source-attributed claims determine citability in financial queries |

| Visibility Score | How frequently your brand appears across ChatGPT, Perplexity, Gemini, and Google AI Overviews | A high score on one platform masks absence on others — fintech buyers research across multiple AI engines before a procurement decision |

Scores below 40 in any dimension indicate that AI models have a structural reason to skip your brand, regardless of product quality.

How to run your diagnostic in four steps:

- Go to GEO Score Checker

- Enter your brand name or domain

- Receive your four-dimension scores within 60 seconds

- Identify the lowest score — that’s where your citation gap is largest

The scores are comparable across competitors. If your Bot Access reads 22 and a rival fintech reads 74, you’re not competing on equal footing in AI search, regardless of your actual product capabilities.

What Fintech Buyers Actually Ask AI Before Signing a Contract

Procurement-grade fintech queries are already flowing through AI platforms at scale. According to a March 2026 analysiscovering 680 million AI citations, 73% of B2B buyers now use AI tools in their research process. In fintech, where deal sizes average $50K–$500K+, a single missing citation can cost a qualified pipeline entry.

These are the prompts your buyers are typing:

| AI Prompt Example | Platform | Search Intent | What It Reveals |

|---|---|---|---|

| “Best payment orchestration platform for enterprise SaaS” | ChatGPT | Vendor shortlisting | AI prioritizes brands with technical depth indexed in trade publications |

| “Which embedded lending APIs are PCI DSS compliant?” | Perplexity | Compliance verification | Perplexity checks community sources; brands absent from r/fintech lose citation weight |

| “Compare fraud detection tools for neobanks in 2026” | Gemini | Competitive evaluation | Gemini favors website-native content with clear comparison structure and schema |

| “What compliance certifications should a B2B payments provider have?” | ChatGPT | Risk assessment | .gov references, FINRA mentions, and inline disclaimers in content drive citation authority |

| “Best treasury management software for mid-market companies” | Perplexity | Active procurement | Perplexity surfaces brands cited in Banking Dive, American Banker, and LinkedIn content |

| “Is [your brand] regulated by the FCA?” | Google AI Overviews | Trust verification | AI Overviews pulls from structured regulatory data — missing Organization schema means no answer |

If your brand doesn’t appear in responses to these prompts, you’re not losing awareness. You’re losing active buyers who have already decided to purchase and are now choosing between vendors.

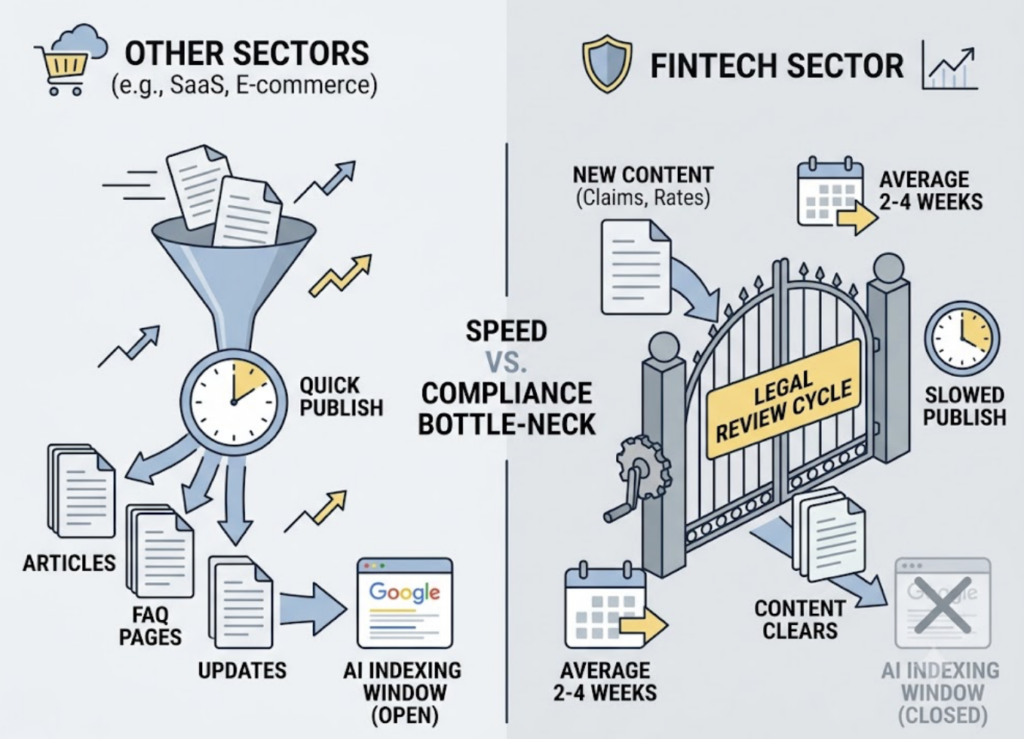

Where Fintech Brands Consistently Lose GEO Points

Fintech has a specific GEO problem that most other industries don’t: compliance teams slow content production, and that structural bottleneck compounds over time.

In sectors like SaaS or e-commerce, brands fix GEO issues by accelerating content output — more articles, more FAQ pages, faster publishing cycles. Fintech can’t do that cleanly. Every piece of content that touches product claims, rate disclosures, or regulatory coverage goes through legal review. That review cycle averages two to four weeks in most mid-sized fintech organizations. By the time content clears compliance, the AI indexing window for a trending financial query has often closed.

The result: technically weaker competitors that have invested in structured data infrastructure — proper schema markup, open bot access, clean entity signals — consistently win citations over more credentialed brands with slower content pipelines.

That’s not a content quality problem. It’s a GEO infrastructure problem.

The other pattern is YMYL authority decay. Financial content that was authoritative in 2023 often lacks the inline disclaimers, source attribution, and named author credentials that 2025-2026 AI models now require for citation consideration. A product page that reads “rates starting from 8.9% APR” without a regulatory source embedded in the same sentence scores lower on Content Signals than a page that reads “rates starting from 8.9% APR per the Key Fact Statement required under FCA guidelines.” Same product information. Different citability.

| Fintech Scenario | GEO Score Signal | Likely Cause | Action Direction |

|---|---|---|---|

| Compliance pages not indexed by AI | Bot Access: <30 | GPTBot/PerplexityBot blocked in robots.txt or via Cloudflare rules | Audit bot-specific crawl permissions separately from Google |

| Product pages missing from AI comparisons | Structured Data: <40 | No FinancialProduct or LoanOrCredit schema; generic Organization schema only | Add financial-specific JSON-LD fields including regulatory metadata |

| Cited on ChatGPT, absent on Perplexity | Visibility Score: split | Brand presence concentrated in publications ChatGPT favors; no Reddit/community footprint | Build citation presence across r/fintech, Banking Dive, and LinkedIn thought leadership |

| Content exists but doesn’t get cited | Content Signals: <45 | Inline disclaimers absent, no named credentialed authors, rate data not source-attributed | Embed regulatory source references within the same sentence as financial claims |

From a One-Time Score to Continuous GEO Monitoring

The GEO Score Checker gives you a diagnostic snapshot. It tells you where your fintech brand stands today across four dimensions.

That snapshot matters. But fintech AI visibility changes continuously. Regulatory updates shift AI trust signals. A competitor earns a citation in American Banker, moves up in Perplexity’s weighting, and displaces your brand from a vendor shortlist query. Your compliance team publishes new risk disclosures that, if properly structured, could lift your Content Signals score by 15–20 points.

A one-time score doesn’t catch any of that.

Topify’s Comprehensive GEO Analytics tracks all four GEO dimensions continuously, with per-platform breakdowns and competitor benchmarking. For fintech brands where a single enterprise contract can run $200K+, knowing which direction your AI visibility is trending — not just where it sits today — changes how you prioritize GEO investments.

| Capability | Free GEO Score Checker | Topify Platform |

|---|---|---|

| Check frequency | One-time snapshot | Continuous monitoring |

| Dimensions tracked | 4 GEO scores | Full GEO analytics + sentiment + citations |

| Historical trends | None | Full trend history with alerts |

| Competitor benchmarking | Not included | Real-time competitor tracking |

| Platform breakdown | Aggregated | Per-platform (ChatGPT, Perplexity, Gemini, AI Overviews) |

| Optimization actions | Directional guidance | Specific, prioritized execution steps |

Plans start at $99/month with a 7-day free trial, no credit card required. See full pricing details to compare tiers.

Conclusion

In fintech, trust is the product. AI models apply that same logic: they cite brands whose technical signals demonstrate verifiable authority, not just brands with the best products or the largest marketing budgets. If your Bot Access is blocking compliance crawls, your schema markup is missing financial-specific fields, or your content lacks inline regulatory attribution, your GEO score reflects that — and so do your AI citations.

Start with a free GEO score check. Four scores, 60 seconds, no account required. You’ll see exactly which dimension is creating your largest citation gap.

From there, use Topify’s AI Robots Checker to audit which bots can actually reach your compliance and product pages, and the Brand Authority Checker to see how AI models currently assess your financial authority signals. For a cross-platform visibility snapshot, the AI Visibility Report shows where you stand across ChatGPT, Perplexity, Gemini, and Google AI Overviews in a single view.

Frequently Asked Questions

What is a GEO score, and why does it matter for fintech brands?

A GEO score is a 0-100 composite rating that measures how well your website is optimized for AI search engines like ChatGPT, Perplexity, and Google AI Overviews. For fintech brands, it matters because AI models apply YMYL (Your Money or Your Life) standards to financial content — the bar for citation is higher than in most industries. A low GEO score means AI can’t verify your regulatory authority, structured product data, or content credibility, so it skips your brand in favor of competitors whose signals are cleaner.

Why would a fintech site score low on Bot Access?

The most common causes are robots.txt rules that inadvertently block AI-specific crawlers like GPTBot, ClaudeBot, or PerplexityBot, and Cloudflare or WAF configurations that rate-limit or challenge non-browser traffic. These rules are often inherited from security policies designed to block scraping, but they don’t distinguish between malicious bots and legitimate AI crawlers. The result: your compliance pages, product specs, and licensing data become invisible to the AI models your buyers are using.

Does having good Google SEO mean a high GEO score?

Not necessarily. Google SEO optimizes for ranking signals — backlinks, keyword density, page authority. GEO optimizes for citation signals — structured data quality, bot accessibility, content authority markers like named authors and inline disclaimers. A fintech brand can rank on page one of Google while scoring below 40 on GEO, particularly on Structured Data and Content Signals, because financial-specific schema (FinancialProduct, LoanOrCredit) and YMYL compliance formatting aren’t standard SEO priorities.

How often should a fintech brand check its GEO score?

A point-in-time check with the GEO Score Checker is useful as a baseline diagnostic. That said, fintech AI visibility shifts with regulatory updates, competitor content moves, and changes in how individual AI platforms weight citation sources. In practice, monthly spot checks catch most significant drops. For brands in active growth phases or regulated market expansion, continuous monitoring via a platform like Comprehensive GEO Analytics gives a more accurate picture of where citations are being won or lost.

Which GEO score dimension is hardest to fix for fintech companies?

Content Signals tends to take the longest to improve in regulated fintech environments. Fixing Bot Access is largely a technical configuration task. Structured Data can be addressed by a developer in days. But improving Content Signals requires updating existing content with named credentialed authors, inline regulatory source attribution, and compliant risk disclosures — and every piece of updated content typically needs legal review before publishing. That review cycle is the structural bottleneck. It’s fixable, but it requires coordination between marketing, legal, and compliance teams that most fintech brands haven’t built yet.

Read More: